Workplace accidents and occupational diseases cause significant damage and losses to individuals, communities, and the State. There are several methodologies for quantifying them. For these calculations to be valid, they must not overlook the question of who bears these costs, identifying the individuals and groups who suffer the damage and its consequences.

This article will attempt to establish the true costs of accidents at all levels, that is, not only at the business level but also their social cost.

Traditionally, companies have considered security as an expense or one of the costs that the business must assume. However, many modern managers view and treat security as an investment, one that can have significant returns, both human and economic.

More than 50 years ago, H.W. Heinrich, a pioneer in safety management thinking, wrote in his influential book, Industrial Accident Prevention, that "the most valuable methods of accident prevention are analogous to the methods required for controlling the quality, cost, and quantity of production." At the time, Heinrich's thoughts in this regard received little attention due to the emphasis placed on reducing accident rates. But in recent years, a significant number of major organizations have discovered that applying the tools and techniques described for Loss Control has brought them not only greater safety but also measurable improvements in efficiency, quality, and productivity.

When we analyze the costs of workplace accidents, we can see that they exist in two very different ways. On the one hand, we find the social and human repercussions, costs, or losses, and on the other, the economic ones. From an ethical and moral perspective, the human cost of accidents is more than enough reason to combat them. We are all obligated to take all necessary measures to prevent them from occurring. The suffering of those injured and their families is the most powerful reason to fight against workplace accidents.

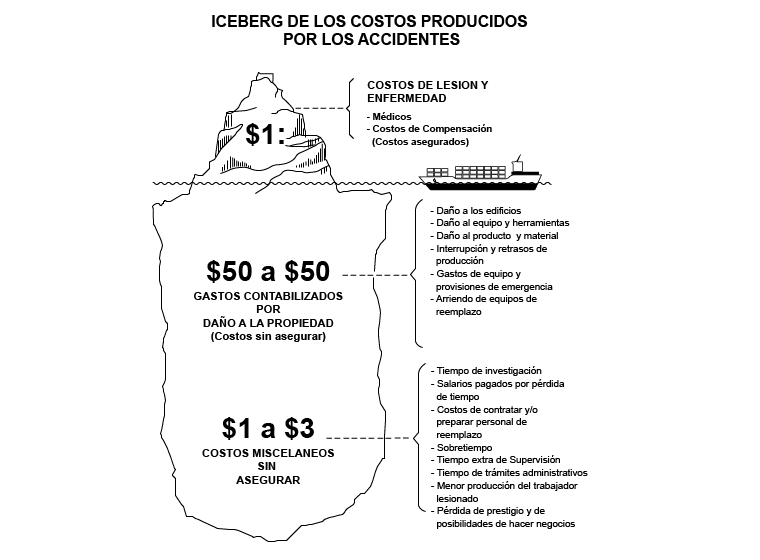

THE ICEBERG OF ACCIDENT COSTS

Every accident means higher operating costs for companies, whether from legally imposed contributions, such as benefits to finance workers' accident insurance and fines, or from costs derived from unproductive expenditures due to deterioration of materials, products, equipment, lost time, etc., which constitute the indirect costs of accidents, also known as hidden or invisible costs because they are difficult to quantify. Studies on the subject conducted by experts indicate that indirect costs are at least five times higher than direct costs.

When we talk about workplace accidents and occupational diseases, it's not uncommon to find that, when faced with pressure to undertake an investment, business owners and managers argue that it would be very expensive and, therefore, "impossible." Nor, on the other hand, is it unusual to hear the usual response from prevention specialists and labor representatives, who argue that workplace illnesses and accidents also represent a very high cost for companies.

But how effective are these economic arguments in convincing, in the preventive sense? To facilitate the argumentation in the conceptual realm of economics, we will review, step by step, some partial aspects. Then, at the end of this section, we will address the question: Who pays the economic costs of accidents and illnesses?

What are we talking about when we refer to the costs of work-related accidents and illnesses? First, we must address the following two aspects:

THE COST OF SECURITY FOR COMPANIES

Direct costs in the European Union alone are estimated at an average of €22 billion annually. It is very important for companies and nations to know and control these costs, in order to have an accurate understanding of them and the accidents that cause them, and thus be able to manage them. Furthermore, they often constitute a decisive argument to convince all those employers and workers who consider Risk Management or Prevention not just a nuisance, but a useless expense. Nothing could be further from the truth.

Security costs for companies have several components which can be expressed as follows:

1. THE COST OF PREVENTION

To combat accidents and illnesses, we must first understand their underlying causes. When the causes are inadequate equipment or facilities, investments in their renovation are required. These investments are often costly, but they are also often unavoidable. For example, when faced with an outdated electrical system inadequate for the load it supports, there is no choice but to replace it. The paradox is that what will happen when the investment is made is that economic results will improve because there will no longer be unproductive downtime due to power outages caused by overload. This example illustrates that prevention costs cannot be separated from production costs. In this sense, we can say that the majority of prevention costs must be considered productive investments and, therefore, are profitable investments, not just expenses. Furthermore, in many cases, these prevention costs are transformed into productivity for the company. The same can be said for any health improvement that involves technological upgrades. It's quite possible that, thanks to the requirement to comply with noise or dust pollution regulations, for example, the company will see increased productivity and profitability.

2. THE COST OF ACCIDENTS

The second type of argument usually revolves around how much money the company loses when accidents or illnesses occur. Here, the "preventionist" idea is usually that the larger the true cost we can demonstrate to the company, the more the concept of prevention will be taken into account. For these purposes, the argument is that attention must be paid to the fact that, in addition to the obvious costs (also called visible) there are a whole series of hidden costs (called invisible) that the company assumes, even if it doesn't know it. These costs are due to the impact of accidents and illnesses on the company's normal operations, which generally entails a decrease in production, sales, or a deterioration in the quality of the company's products or services, etc., and this means economic losses for the company and, of course, money. The idea here is that if the company were to keep a detailed accounting of these costs, it would conclude that prevention is very important.

Some examples of invisible or hidden costs are salary costs paid to the injured worker or his replacement, costs for loss of equipment or materials, sales or customer costs and of course damage to the company's image.

3. THE COST FOR WORKERS AND THEIR FAMILIES

The economic cost to workers and their families is defined as the damages caused by work-related accidents or illnesses that go uncompensated. Leaving aside, for a moment, the impossibility of compensating for moral damages, the compensation received never covers the true economic costs. Workers bear an economic cost, whether through a reduction in their income, damage to their future employment prospects, or a loss of their ability to work. Added to these costs is the economic impact on the families of the injured, who take on the responsibility of caring for them, without financial compensation.

4. THE COST TO PUBLIC ACCOUNTS OR THE STATE

The costs of accidents and illnesses not borne by businesses or individuals are transferred to public accounts. For example, the costs of workplace accidents not declared as such are covered by the public health system or the State, as if they were common accidents.

5. THE SOCIAL COST

The costs to the public purse do not exhaust the costs to society. There is currently no accepted way to calculate the costs and benefits of health and safety or accidents and illnesses in monetary units. Partly because it is arbitrary to assign any quantitative value to intangibles, and partly because of the multiple relationships that health has with any other social aspect, it is almost impossible to model the quantitative relationship between cause and effect (if we accept that health, social well-being, or quality of working life are social goods, an analysis of the costs and benefits to society of safety should be able to take them into account).

CONCLUSIONS

REFERENCES

https://camiper.com/investigacion-por-camiper-escuela/el-costo-economico-de-los-accidentes-laborales